indiegogo-kite-patch

Pitch your Startup, App or Hardware or post a Startup Event or Startup Job

This article is one of a collection of articles on Crowdsourcing published this week, you can find the others here – Crowdfunding Articles

Ian A. Maxwell is a veteran Technology Entrepreneur and Venture Capitalist. He is currently CEO of BT Imaging, Chair of Instrument Works and Co-Founder of Accordia IP as well as a partner at Zetta Research and an Adjunct Professor at RMIT. He has a PhD in Chemistry and has either founded or worked at Memtec, Allen & Buckeridge, Redfern Photonics, Sydney University Polymer Centre, James Hardie, Viva Blu, Enikos, Wriota, RPO and Instrument Works. You can connect with him on Linkedin au.linkedin.com/in/maxwellian

David Drake is a leading equity expert based in New York. He is the founder and chairman of LDJ Capital, a private equity advisory firm and founder of the Soho Loft an events company that produces and sponsors 150+ global events a year on topics such as Crowd Funding, Venture Capital and finance reform.

Mike Nicholls is a Director of a US based Investment Fund, has started and sold businesses and publishes Startup88.com

Andrew “Wardy” Ward is a Sydney based serial entrepreneur who has founded at least 5 businesses including the well-known “3 Minute Angels” and a technology outsourcing business based in the Philippines and is currently preparing a submission to the Corporations and Markets Advisory Committee on changes to the Australian Federal Corporations Act to facilitate Crowd Funding.

This article came about after Ian and Mike were discussing Crowdfunding over a beer, Ian arguing that he didn’t like it and me arguing it was a positive thing albeit with new risks, so we decided to flesh it out and got an International Perspective from David and a local perspective from Wardy.

Risks of Crowdfunding

Ian: There are two broad classes of crowdfunding for tech start-ups:

1. Product funding prior to product development and/or product release

2. Micro-equity funding

I am wary of crowd-funding but very interested in it as an experiment. Most modern tech start-ups are working in areas where the ideas are innovative, but not inventive under patent law. This means it is hard, if not impossible, to get patent protection for products. One issue with seeking crowdfunding prior to actually developing and/or releasing a product is that you give away the innovative idea to other entrepreneurs and corporations, who can then run with the same idea.

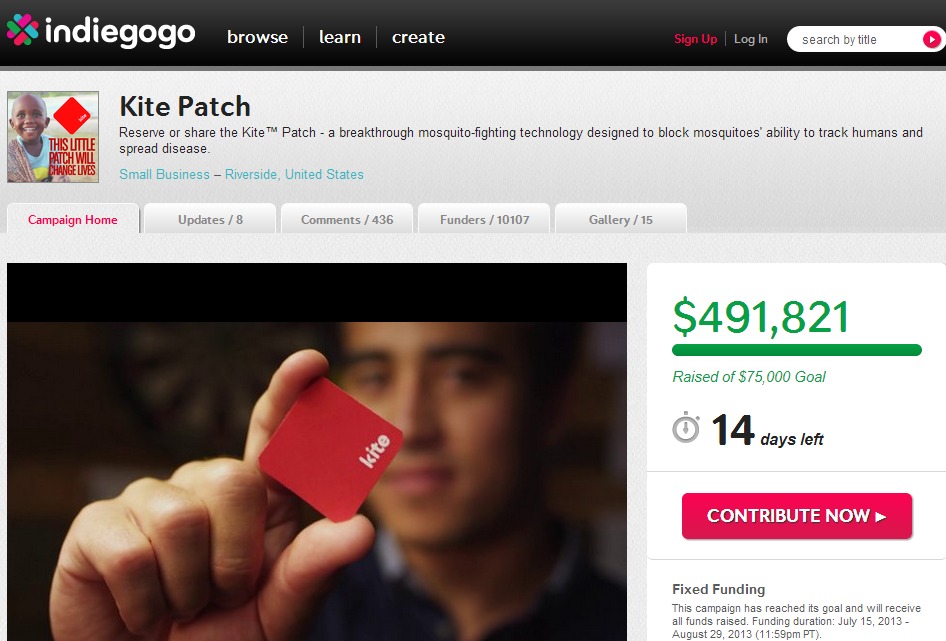

Mike: This is true, however the vast majority of startups are execution plays not IP plays, very few of the crowdfunded campaigns have created truly inventive products where a patent would be granted (the Kite Mosquito patch is an exception but this was in the Universities years before) . Patents take 3-5 years to be allowed and generally speaking they are not particularly effective as a weapon to defend a small startup.

Ian: I think we are saying the same thing here. The issue with publicizing your product concept before you have produced it is quite a risk, and the risk is that someone else might say ‘thanks for the idea’ and execute the idea better than you can. This is especially the case when you have no patent protection to fall back on, for either protection of product margin or market share, or to hold up your enterprise value in an M&A transaction.

Wardy: Clearly crowdfunding is telling people about your idea pre-money and pre-product. Yes anyone can then latch on to that idea and then develop it (if they have funds). But these same copiers will not have a crowd of supporters and if they are funded in a position to latch onto other people’s ideas, they would have copied anyway, so better to go to market with a fan base.

Aside from those startups that have intellectual property which may be patentable, (not that suitable for crowdfunding), in my opinion crowdfunding offers most tech plays an advantage on balance. Because crowdfunding’s popularity suggests there is abundance of ideas (ideas are possibly a commodity) and it is execution, marketshare, customer base and momentum that matter most to tech plays. These factors make tech plays that have originated from crowdfunding generally safer / better investments.

Ian: Agreed – many innovations are almost born as commodities – crowdfunding really only exists because so much product development can be outsourced these days, mostly all of it in fact. For example I have just bought a new bicycle seat of Infinity Bike seat off Kickstarter. I would say that if it has any merit that the incumbents will be copying this design very shortly. The bloke who formed the company has totally outsourced production, but he has a very small window of opportunity to develop a sustainable company. Its really a project and it might, just might become a company,

Debt vs Equity

Ian: I think that crowd-funding for future product development or delivery represents a ‘debt’ owed by the company. This represents a drag on future cash flows and also a restriction of strategic flexibility. There is a good reason why startups traditionally get funded through equity investment prior to product sales, and this is so they can spend all the money they have on accelerating their path to sales and achieving Cashflow positive status. In addition, once having taken cash for products the company is less free to change directions if it finds new competition, technology challenges or better opportunities.

Mike: Agreed, but if you have priced the product properly and the crowdfunds are released to you to complete and produce the product, there is no drag, quite the opposite. If you are launching a crowdfunding campaign without a prototyped product that is nearly ready to make then you have a major problem that could easily come off the rails. I understand Kickstarter has introduced a policy of requiring hardware prototypes to have been built prior to launching a new campaign which makes a lot of sense, Ian as you know better than anyone hardware is hard. A successful Kickstarter gives you your first 1000 or so customers who will most likely be more forgiving than someone buying in a shop.

Wardy: Using pledge-based or rewards-based crowdfunding pre-sold product business do create a ‘debt’, but where legislation is allowing CSEF then it is not a debt – its equity. It has the same economic advantage of direct equity investments by Angels or VC’s, but comes with additional practical benefits like the crowd of advocates.

Mike: I disagree, its a short term liability not equity regardless of the legislation there is no equity being issued (in some cases there is no legal entity, its an individual or a business name), however for all intents crowdfunding provides a very similar risk profile to equity for the startup without having to give up potentially valuable equity and I am fairly certain that most crowdfunding pledgers don’t expect to see their money if the campaign falls over nor is it likely they would ever take winding up action like a large debtor that has not been paid.

I am not aware of any major cases going through the courts in any jurisdiction as yet. Also there is no upside for the crowdfunder, in fact it is very biased to the entrepreneur but I think this is a good thing, if the product is popular, its a very cheap way to test the market to see if there is appetite without having to launch a business and build a product, factory etc. Content spruikers have been doing this for decades, describe a content product if enough people buy into it, produce the content. There have been many experiments with books as well, Stephen King was giving away the 1st chapter of new books and only completing the book if there was demand.

Wardy: As for crowdfunding making the business less nimble and able to respond to the evident changes required in their business plan – I can see how that could be true. My personal experience is that with polling and communication to the crowd you can assess the relative benefits of changes to strategy, which makes sense when its rapidly changing landscape such as tech. If the crowd thinks your change sucks it probably does or conversely if they think it’s a winner they will back that too.

Perhaps this is just my experience, but I have found Angel investors nail down the entrepreneur to a defined business plan that everyone buys into. The Angels I’ve had (I’ve never attracted VC money) are very reluctant to move (quickly) from the agreed business plan because it changes the management KPI’s and investment boundaries they committed to in the cool rational light of pre-money. I guess that is Investor specific.

Ian: I would agree that Angels are the lowest in my list of preferred investors. I invest in other people’s companies but only where I can take an active role in the operations of the business. I don’t see this as Angel investing.

Advantages of Crowdfunding

Marketing

Ian: One of the key benefits of product crowd-funding is its use as a form of marketing to geeks and early adopters when the product development is just about completed. Its a nice way to get your product noticed by a certain sort of person. But promoting a concept too early in it’s development phase is not always such a smart idea as I have mentioned above.

Mike: In the early days of Kickstarter it was about the funding to get something built, now most companies I talk to see it as much a marketing and product launch as raising the funding, in fact many of them often have Angel or VC funding, it has become an extremely effective way of getting a cool product market tested and in many cases where it is newsworthy major press coverage.

Crowdfunding Equity

Ian: I am unsure about micro-equity crowdfunding. Almost undoubtedly there will be a few winners under micro-equity crowdfunding schemes but many, many losers. I suspect that the return on investment (ROI) for investors will look like a very skewed Gaussian distribution with a small number of high returns, a handful of medium returns or ‘money back’ for investors, and a long tail of investors that lose all their micro-investments. (sounds like VC except there will be returns J ).

My guess is that this form of asset class will be loss making overall (negative ROI) simply because it is venture capital without the benefits of venture capital selection and mentoring (almost like Australian VC in fact, which has a long term negative ROI). This would mean that any committed investor would, the longer they invest, revert to the mean, i.e. have a loss making position. After a period of time any asset class which are loss-making (adjusted for risk) disappear.

Wardy: Did you say the Australian VC industry (my market) has a long term negative ROI? If that is true then crowdfunding should surely be used as tool to move this into positive for the VC’s by vetting and de-risking crappy deals so that the only ones they are exposed to is the medium and hot stocks. There is no reason a VC would come in a later stage and invest in an under-performing crowdfunded entity. Is it also true that the Silicon Valley VC industry has negative ROI, like the Australian one? Asked in genuine ignorance.

Ian: Australian VC historically has had a negative ROI. Tier 1 Silicon Valley VC is actually above the 20% ROI hurdle, i.e. profitable on economic basis. I have just written an article on the problem in Australian VC, but a quick summary is that the problems are people, fund scale, fund model and deal flow. My feeling is that equity crowd-funding would not solve these issues. But that is a guess only.

Mike: I also think that we have had such a small number of VCs In Australia with such small total funds and numbers of investments that it is statistically non valid, the sample size is too small.

Ian: I don’t know – the data I am looking at has 37 funds between 1985 and 2007, with a mean negative ROI for the lot of them.

David: Yet, we are seeing a lot of crowd funders and online VC structures replicating the single purpose vehicle structure that VCs have used for decades. OurCrowd, Seedinvest, Seeders.co.uk, and Funders club are the new players and more are coming. Some leading firms realize that there needs to be a lead investor.

Wardy: It’s my view that crowd-funding has a sweet spot between $50k-$100k and approaches limits (regulatory, practical and otherwise over $500k). This puts them in a different stage of funding to Angels and VC’s who enter on deals above that value. Equity crowdfunding is thus a feeder to established investment networks/channels. It sits further up the pipeline.

Mike: I don’t believe we should have purely crowd funded deals. I think we need a hybrid between a professional investor as the lead investor and crowdfunding to make up the volume of the round.

Venture Capital has been pretty broken in Australia for much of the 15 years I have been in around the startup scene. I believe that we will see Super Angels, who otherwise could have been Venture Fund managers, decide to start leading rounds with Crowdfunding taking the rest of the round.

In my opinion the following is an ideal scenario

-

Lead Investor leads $500k round, could be an individual or advisory firm but must put their money where their mouth is.

-

Lead Investor does the due diligence.

-

Crowd Funders follow with $500k-1m.

-

Lead Investor picks up a small capital raising fee for the funds raised

-

Lead Investor is the Director on the board representing the Crowd

-

Lead Investor picks up a similar MER to a VC for managing the Crowds money (this is reasonable in my opinion and is most likely thing to stop crowds being ripped off)

-

Lead Investor gets an extra % of carry for leading the round and sitting on the board.

-

If the lead investor is successful they will have more people willing to back them

This could in fact be a great way for smaller VCs to leverage their funds by allowing Crowdfunders to back them and to still earn income on the management fees.

Increasingly good entrepreneurs who have had successful exits will reject traditional 10 year VC Fund cycles and the pain of raising a fund (especially in Australia where many have failed to raise funding even when backed with Government IIF funds). The flexibility of a crowd model means not having to raise another fund, simply find a great deal, do the due diligence put it up on a crowdfunding platform, do a deal, if you have been successful then the crowd will back your judgment and put their money behind yours. You earn a higher management fee and carry for the work, potentially it could be similar to the management and carry structure of a traditional fund.

David: I have been advising angel networks for over 2 years to embrace crowd funding and become the lead investor of crowd funded campaigns. The UK has accomplished this with Syndicate Room that has now been operating for over a year. Business angels take a lead investment of at least 25 percent of the raise and crowd funders and other angels can co-invest under the same terms. They just closed a £590,000 investment.

Ian: It’s clearly early days and what you are describing is the start of an experiment. Micro-equity crowdfunding looks to me like venture capital with a few positive attributes removed For some its simply a source of cheaper and dumber money. If someone can come up with a mechanism to overcome some of the potential issues, as Mike has suggested (e.g. placing a ‘rating’ on entrepreneurs so the punters are making more informed bets) then maybe things might work out. Having said all that if the whole thing is promoted as a ‘gamble’ managed through the betting shops alongside the horses then maybe it will take off anyway. Compared to investors, gamblers subconsciously do expect to revert to the mean of a negative ROI.

Wardy: Through the lens of a VC there would be two types of deals, good ones and gambles. But through the eye’s of a CSEF-nut like me there are 2 types of experiences: the ones I have when i interact with other people’s businesses and the experience I have when it’s “my business” (no matter how small your equity stake or voting rights, the experience of “mine” is huge). Having more people buy in to an idea has a value in “network effect” that mysterious “network effect” must have value otherwise the prices paid for successful tech plays Tumblr, Twitter, Snapchat etc are a ruse.

Ian: I get that – if the primary intention is have fun and be recognised as part of the ‘club’ then I think this model will be a roaring success. I also recall it took a few cycles, 3 or 4, for the current VC model to settle down into something worked. All the negative scenarios had to be understood and then factored out – this is what you see in standard deal docs. It might take a few cycles for crowdfunding to get sorted too.

Crowdfunding vs VC

Ian: Good VC in Silicon Valley has very special due diligence and supervisory skills. One, a very defined means to select investment based on years of partner specialization in a market segment where they know all the corporations that are buying companies, where they have worked themselves in both corporate and start-up CEO roles. Two, ability to mentor company including finding valued co-investors, new CEO’s and other management, board overview and strategic input, and exit guidance, introductions, and execution. Three, VC’s solve problems with excess capital (in the US).

Mike: Yes this value add is what is expected of the VC, I am not certain this happens in real life.

Ian: I expect to see a lot of micro-equity crowdfunding pop-up, especially where there are tax incentives for investor/gamblers (as in the UK). Remember it takes ten years or so to assess the value of a new financial asset class, and even longer if there is a macro-economic event (like a GFC) to confuse the results. I honestly hope that a sensible model does emerge for micro-equity crowdfunding, but you have to remember that there is already too much VC money in the market. Adding micro-equity crowdfunding to the mix will simply depress financial returns for all investors because what doesn’t change is the M&A/listing value of the sum of all the exits – you simply can’t make quality exits by pumping money into the front end creation of start-ups (because quality deals rely on a fixed quantity of quality entrepreneurs). Just for clarification here – across the whole market for start-ups the amount of money going into the sector simply has to be less than the total value of all start-up exits, or else the asset class is loss-making.

Wardy: Is the whole asset class of tech start-ups (incubated, funded and matured the way they are) loss making?

Ian: For the last decade, yes, VC globally has been loss making simply because too much capital was committed to VC early in noughties when LP’s got a little over excited. We are still working through this overhang of excess VC capital and excess availability of new technologies.

Wardy: Also, I’d make the point that the destiny for many crowdfunded business (unlike tech startups) is not to be listed or trade-sold in 3-5 years. Many crowdfunded ventures will be products of a tangible nature, niche servicing businesses and local businesses that are sourcing equity and customers concurrently.

Ian: None of the key VC characteristics will available for micro-equity crowdfunded deals so one would expect a much lower quality of return on investment. In fact it could be worse than expected since the deals that go to micro-equity crowdfunding might in fact be the deals that are sensibly rejected by VC. Another by-product of not having VC mentoring is that entrepreneurs will not learn much by failure, and hence the current rule that ‘5 failures of a founder will lead to the sixth success’ will be broken.

Wardy: Might be just me, but if the Australian VC industry has negative ROI, the average Silicon Valley VC has negative ROI and the whole asset class of tech start ups is loss-making, then the business model for finding and funding of these businesses isn’t economic and the VC’s are either not adding the value they believe they are or tech startups is not a good investment with or without crowdfunding playing a role.

Surely Ian can’t be saying VC’s do a good job of vetting, funding and accelerating ventures if my understanding of what he has said (negative ROI for the asset class) is correct?

Ian: Tier 1 VC is good. The overall problems in the sector is that Tier 3 in the US and VC in Australia isn’t anywhere near as good. So one can’t paint the whole asset class with the same brush.

Mike: I agree deal quality and due diligence is a big issue in a crowdfunded deal (as it is in any deal) which is why I think we need a Lead Investor with crowdfunding backing him up.

Ian: Yeah the problem here is that I, for one, as a lead investor don’t want to deal with a bunch of micro-equity crowdfunding punters as co-investors and shareholders. I would prefer to deal with one or a small handful of professional investors that I know and trust.

Mike: What if there was a reward for this which provided a similar financial result for you as running a VC fund (ie carry and management fee) without the pain of trying to raise a fund. It would certainly be more flexible and nimble. At some point this would make financial sense and for you it would lead to leverage you can’t get on your own.

Angellist is running a similar concept called Syndicates

Ian: I would have to trial it first before I answer that, or better still watch someone else trial it!

Ian: There may be a disconnect between entrepreneurs and their source of capital. It is human nature to take more care of capital if one knows the individuals representing that capital personally and they are sitting on your board. I expect micro-equity crowdfunded companies to be looser with their fiscal or operational responsibilities.

Wardy: The counter argument is that the crowd minimises the risk of a person being fiscally irresponsible because it is shared with many people if they are. I’ve known many mates who don’t talk about being ripped off in deals where only a small number of people are players because they feel personally embarrassed at having been swindled. A crowd thats embarrassed feels rage not shame. Pity the repeat crowdfunders that are fiscally irresponsible.

Mike: These are reasonable concerns, again having a known lead investor with their own money invested should resolve some of these issues. Also if there is a platform to facilitate the management and corporate Governance of investees companies will be forced by the platform to adhere to the funding rules.

I see a crowdfunding platform which does the following

-

Allows a business to create a fund raising IM (in a standardized template so that they can all be benchmarked)

-

Allows Lead Investors to sponsor a deal (somewhat like a Broker/Underwriter) does for an ASX listing, these would be their mentors and then board directors as well as representing the crowd in critical business matters.

-

Allows comments, questions, ratings by crowdfunders on each deal with funding commitments locked in once committed

-

Perhaps a Lead Investor could have two director seats, one for himself and one for the Crowd

-

The crowd could vote to remove a Lead Investor if they lost confidence (as normal shareholders do now)

-

The platform could have a messaging facility for each company being required to file updates and financials monthly to the investors via the program

-

The platform and the Lead Investor could develop KPIs an investee company and those are reported on in the monthly update

-

All critical business matters which can be delegated to the Lead Investor will be

-

For Critical Business matters that cannot be delegated, the platform can manage the process of calling a meeting.

-

Potentially this could also handle digital proxy voting and digital voting

Wardy: In relation to the CSEF legislation that Australia is considering chief concern is the way intermediaries can provide processes for Issuers that support governance concerns of Investors. This has yet to be tested in Australia, but I would be interested in the UK experience of governance, disclosure, transparency and Investor confidence in deals. David?

Ian: With many small investors micro-equity crowdfunded companies will have a large administrative burden associated with keeping their investors informed and any process that requires shareholder approval (and there are many of these) will be a logistics nightmare and very expensive. And worse still it will be slow.

Wardy: In most cases the funds and rights of the crowd are pooled to special purpose vehicles that then deal with the crowd-derived investors as a single group.

Mike: I take your point however these can be circumvented by passing a critical business matters provision which the lead investor can exercise for matters such as capital raising, sale of business etc. Again if a crowdfunding platform incorporated a lot of this it would go a long way to solving these issues.

Ian: There are restrictions under corporate law which make many critical business matters subject to shareholder approvals. You can’t get around this at all. And if you try, and the company ever ends up being worth something, you will find yourself in court for ever. Spurious or otherwise, this will happen.

Mike: How about if the platform provided a digitally signed proxy vote?

Ian: One interesting class of finance is Venture Debt. It represents about 10% of start-up funding in the US. This is repayable loan finance to start-ups with high interest. 10% is about the right level since it represents the ceiling of equity to debt levels that mean debt can be repaid with appropriate risk factors and interest rates. Today all venture debt is by managed funds – I think that in the US that micro-equity crowdfunding could be an alternative and cheaper means to raise Venture Debt. I am sure this benefit wouldn’t passed onto start-ups, but in a competitive market you never know. Cheaper venture debt would be a good thing.

Final Words

Andrew Ward: I’ve found the above fascinating. I’ve drunk the “kool aid” (I’m a convert to CSEF) as it were and think that CSEF is a great economic activity because it creates real businesses (often with markets ready to sell and refer), it un-taps investment classes and far from being a gamble reduces risks of investment.

This discussion is focused on tech rather than product businesses and definitely more than local infrastructure projects where I believe the sweet spot for CSEF is.

There appears to be no science to picking winners and exits are few and disproportionate when they come. Voyeuristically watching tech plays and the funding avenues at a entrepreneurs disposal is akin to Survivor. When those entrepreneurs have a high profile its like watching Celebrity Survivor.

If I understood all of the above comments from Ian correctly, this game of Survivor is being played for negative ROI!

If CSEF isn’t embraced by the tech community as a source of good deals and later recognised as a great start to businesses going from “idea to operational”, then I’d be surprised.

However, CSEF is not just a tech play, its about small business, niche business, local business and the experience of “my business”. Crowdfunding businesses not tech start ups is the future for crowdfunding.

The internet, social media and collaboration pieces merely enabled the human or social desire of people to do with their money something of meaning that has instant and delayed gratification in it for them. Hence why crowdfunding will sustain and why so many platforms are springing up.

Investing in crowdfunding platforms is a gamble for instance because of the thousands that have popped up there will be only a few in a couple of years time. If I were a VC looking at platforms to invest in, then I’d be nervous if their core marketing plan didn’t have clearly stated focus to help create real revenue generating business from day 1, like those that sell tangible products or those in the community space (local economics) where the same business model would be rolled out across many geographies. In essence where people would locally crowdfund and locally consume the services provided by that crowdfunded business.

Taking that dimension of tech plays – high rate of failure and applying it to the high rate of platforms that will fail in the next 24 months is not a fair comparison to how crowdfunding will perform as an investment class over the next 10 years. Being a bit uppity, I’d say CSEF has as much reason to be buoyant about its future in the real world investment space than has the tech space. The tech space though I think needs to have a good hard look at itself. So much talent, energy and creativity going to waste. Such a weird sales funnel, subject to Zapfs law, Moores law and eroding financial models. Tech investments are a gamble for VC’s.

So back to how can crowdfunding help tech investors?

Well, in my world I see crowdfunding being pre-seed and seed investment (usually $50k-$100k). The very top of the sales funnel. Crowdfunding sorts the wheat from the chaff.

Usually that money is pre Angel rounds and definitely pre VC. Its where Friends Fools and Family operate if the entrepreneur is lucky.

By definition if a deal has been successful at gathering a crowd of investors it now has advocates for customers and that de-risks these now seed-funded ventures when compared with seed-funded ideas that may be pre-revenue and yet to have a database of customers or advocates.

The crowd weeds out ideas that just aren’t that good and delivers a better quality idea.

But the process also weeds out bad entrepreneurs, they have to make a compelling pitch for a start that convinces people they can execute this good idea (at least to the next stage). They are (country specific) vetted and unable to commit fraud or disclosure breeches – which reduces DD costs for Angel or VC funders. And you have real time evidence of their ability to continue to manage their crowd of investors and show you how they will manage your money and expectations. Finally there is social pressure to perform above and beyond with increased shareholders. Far from being nameless and faceless these shareholders are a community able and willing to talk and so the entrepreneur is going to be “on game”

The risk of enterprise is smaller with crowdfunding being there at the birth of an idea as it becomes real. The risk of entrepreneur is also diminished.

There was mention of the concern about shareholder numbers. But my understanding is that most tech ventures that are crowdfunded don’t take the crowd directly onto their shareholder register and these class of shareholders (the crowd) are pooled for the purpose of keeping the share register friendly for Angel and VC investment down the track.

If that pooled group of shareholders are represented at board level or not would be a decision on a deal by deal basis. But the risk of that representative being a moron is not higher than the risk of an entrepreneur thats had to put his uncle on the books when his uncle gave him his first $50k-$100k seed funding.

Angels and VC’s can then further improve their odds of backing winners by having lead Angels and syndication alongside the crowd. That seems to give investors in the tech space greater confidence.

Ian: What I have learnt from this discussion is that crowdfunding in one scenario might be a funnel for VC, but that it might be more useful for the funding of small niche companies that might never need or want VC funding. These companies are pretty much about great design and they use off the shelf technology & service providers to both design and build their products. If the models for crowd-funding are focused on these latter types of companies then the whole thing makes a lot more sense. The role of crowd-funding is then to help turn projects into SME’s, by the use of financial commitment (to the company or their products) of the pre-converted. Surely the internet, if it has done anything for us, has enabled small companies that are totally ‘outsourced’ to efficiently compete with the large global incumbents and, if so, maybe crowdfunding is their natural source of seed capital.

Mike: The one comment (and this is for you Malcolm Turnbull) I think Australia is too much of a nanny state to provide a functioning Crowdfunding regime. (except if you are in WA, then its ok to sink tens of millions of dollars into Mining Exploration Non Limited’s that sink and get re-listed as Tech companies)

Over the last 10 years Australian politics has become increasingly focused on taking responsibility for every dimension of society and incessant rule-making.

I think we will have trouble with this as a country, I believe we will struggle to pass legislation which provides a real crowdfunding framework and I think the Government will try to enforce some form of adherence to the Financial Services Licensing regime and I think the end result will be a watered down sophisticated investor regime where only accredited advisors can help companies get crowdfunded by a small pool of investors.

In my opinion Equity Crowdfunding will probably have to happen in some other country like Singapore that is trying to encourage startups and other means to promote growth companies.

It is my prediction that Singapore is going to become the Silicon Valley of Asia, the programs being offered by Singapore’s Economic Development Bureau are miles ahead of Australia in creating a climate that encourages startups and large tech companies to move to Singapore, they also offer a very easy visa program for your family, submit a valid business plan and they will allow you to enter and leave the country as needed for as long as the business is valid. Frankly they also have a very attractive tax regime and apparently are offering very attractive financial incentives to relocate or startup a business there.

If Australia wants to be competitive on a global basis, they should look to beat Singapore.

As always we encourage your comments. Tell us what you think of Equity and Project Crowdfunding in the comments section below

ents.

Pitch your Startup, App or Hardware or post a Startup Event or Startup Job